“It Is a Good Thing That Net Purchases Are Coming to an End Now”

ResearchZEW Study on ECB Net Asset Purchases

The ECB will discontinue its net asset purchase programmes at the end of June. A new study by ZEW Mannheim with the support of the Brigitte Strube Stiftung has examined how the bond purchases have been allocated across the various euro countries.

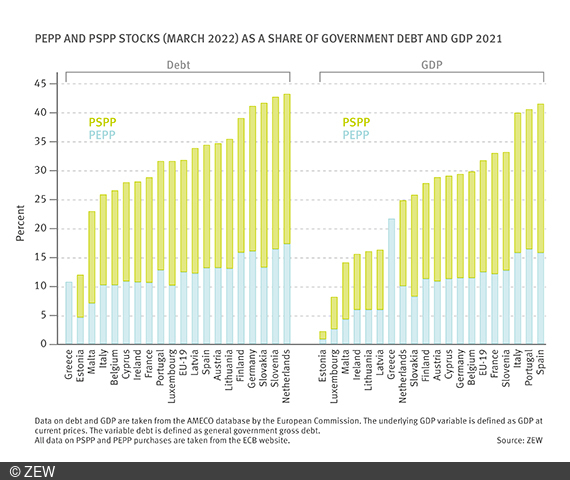

The results show that since the beginning of the pandemic, the share of purchases of government bonds, especially from Cyprus and Italy, under its two purchase programmes, PSPP and PEPP, has significantly exceeded the ECB’s capital key. The PSPP programme has already been active since 2015, while the PEPP was launched in March 2020 to cushion the effects of the COVID-19 crisis. In both programmes combined, the Eurosystem’s purchases of Italian government bonds since March 2020 exceeded the country’s actual share of the ECB capital key by 7.5 per cent. In total, the Eurosystem’s cumulated net purchases of public sector securities reached 4,340 billion euros by the end of March 2022. The purchase shares have fluctuated greatly over time. After Italy and Spain were initially strongly overweighted in spring 2020, their shares had fallen back to a normal level by autumn 2021. Since then, however, the overweighting of these two countries has increased significantly again.

EZB Owns Almost One Third of Euro Government Debt

“Overall, our calculations prove that the ECB has tried to oppose the spread increase on Southern European bonds,” says study author Professor Friedrich Heinemann. “In future, the ECB may indeed continue to reinvest principal payments from maturing bonds for repurchasing those of distressed states. But it is uncertain whether this will be enough to calm the markets,” he says.

Co-author Carlo Birkholz praises the timing of the withdrawal from bond purchases: “It is a good thing that net purchases are coming to an end now, before holdings exceed the critical threshold of 33 per cent of euro government debt. This is an important signal that the ECB does not want to become the ultimate financier of European budgets.”