Economic Forecasts for 2021/22 Remain Optimistic

Business Cycle Tableaus by ZEW and Börsen-ZeitungEconomists Stay Confident

The economic experts are unimpressed by the weakness in growth witnessed again at the beginning of the year. This is the result of the business cycle tableaus by ZEW Mannheim and the German daily newspaper, Börsen-Zeitung. Although Germany’s gross domestic product (GDP) declined by 1.7 per cent in the first quarter of 2021 compared to the previous quarter, the GDP forecasts for 2021/22 remain virtually unchanged. For 2021, the forecast is slightly higher at 3.6 per cent, while for 2022 the median forecast remains at 4.0 per cent. The experts are therefore not revising their expectation of strong economic growth, but merely postponing it.

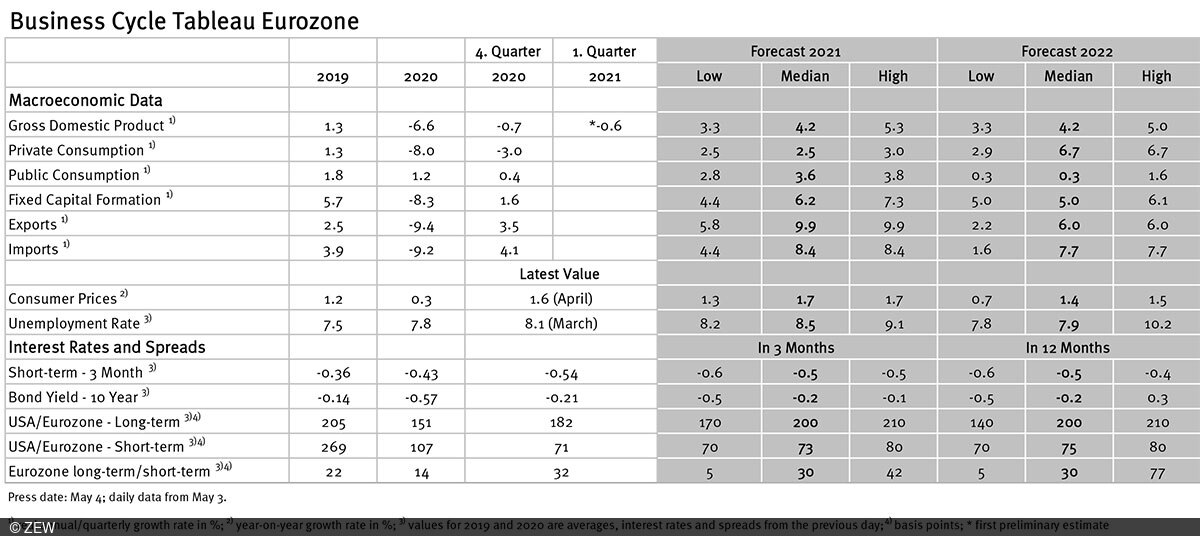

The situation is similar for the euro area as a whole. Eurostat estimates for the first quarter of 2021 point to a decline in real GDP of 0.6 per cent compared to the previous quarter. Since the fourth quarter of 2020 also showed a decline (-0.7 per cent on the previous quarter), this would be a recession by definition. However, given the very positive forecasts for 2021 and 2022, we can hardly speak of a recession. Although the forecast for real GDP has been slightly reduced for the current year, it is still 4.2 per cent (previous month: 4.3 per cent). For 2022, the forecast also remains unchanged at 4.2 per cent.

Economic recovery varies in dynamics

The German economy is expected to recover somewhat less dynamically than the average of the euro area countries. However, German real GDP could still grow more strongly than euro area GDP by the end of 2022 compared to the end of 2019. This is because the pandemic-related economic weakness has so far hit the German economy somewhat less hard than the euro area as a whole. For the end of 2022, German GDP is forecast to be 2.5 per cent higher than at the end of 2019, while the projected increase for the euro area is 1.4 per cent.

No reason to worry about a sustained increase in inflation

The inflation forecasts have also changed only slightly. The inflation rates for both Germany and the euro area have risen significantly, but the forecasts suggest no lasting dynamic upward trend. For Germany, according to estimates by the Federal Statistical Office, the inflation rate for April is 2.0 per cent, 0.3 percentage points higher than in March. For 2021 as a whole, however, the median forecast remains unchanged from the previous month, at 2.1 per cent. In 2022, the inflation rate in Germany is expected to decline again and average 1.5 per cent for the year. Fears of a sharp rise in the inflation rate are thus not confirmed by the forecasts currently available.

Business cycle tableaus by ZEW and Börsen-Zeitung

In cooperation with Börsen-Zeitung, ZEW has been publishing monthly business cycle tableaus for Germany and the eurozone with economic key figures and forecasts since 2013. Numerous banks and institutes publish reports on the current and prospective economic situation at different intervals. The information relevant for the tableau is filtered out of these publications to compute a median, minimum and maximum of the available forecasts for the current and subsequent year.

The monthly tableaus show current GDP forecasts, its main components, consumer prices, industrial production, unemployment rate, short- and long-term interest rates, and interest rate spreads. The focus of the tableaus lies on national business cycle reports, which are complemented with forecasts from international banks and institutes. The tableau for the eurozone is enhanced by data from European banks and institutes.