Between Uncertainty and Positive Signals

Business Cycle Tableaus by ZEW and Börsen-ZeitungEconomic Experts Downgrade Forecasts for 2025 despite Optimism

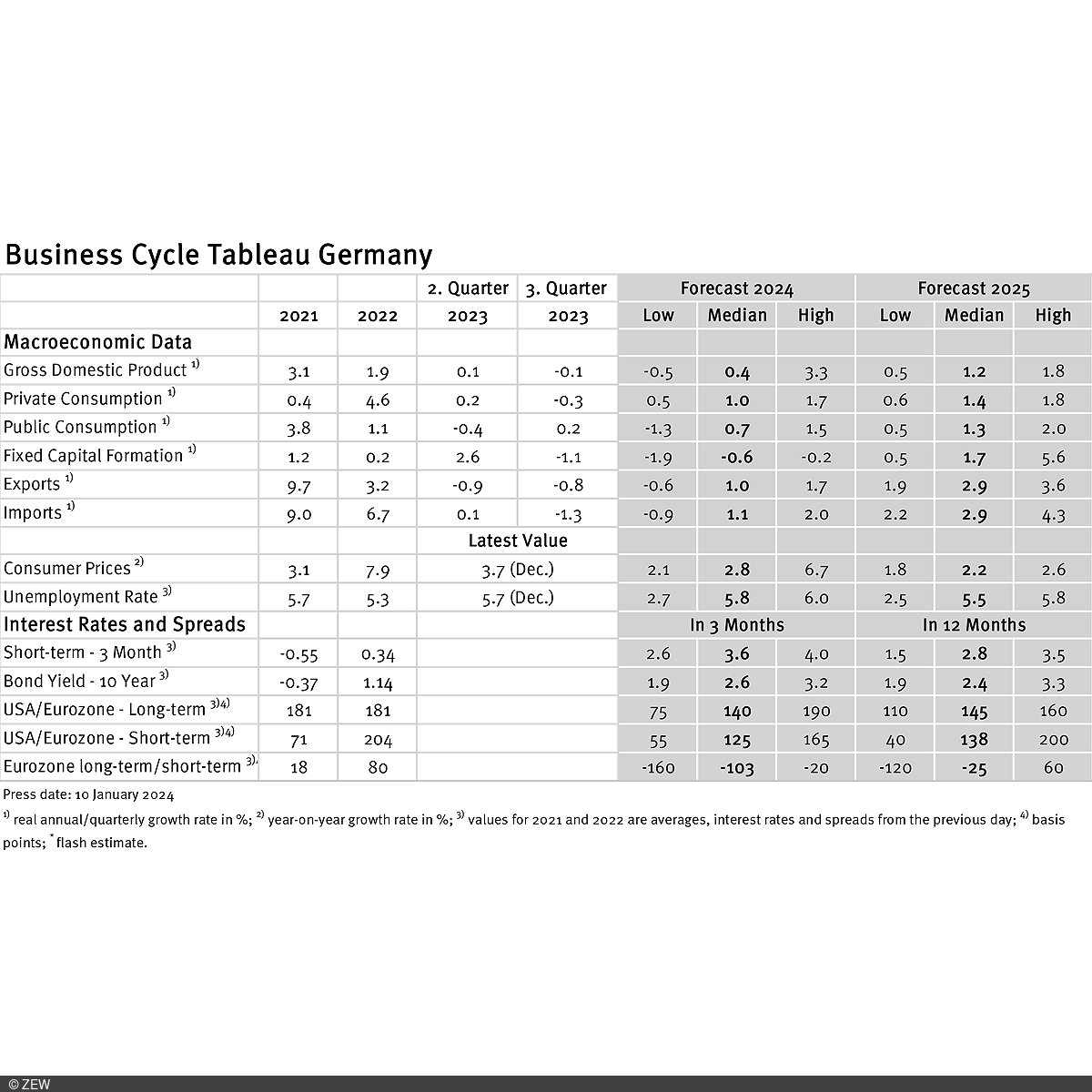

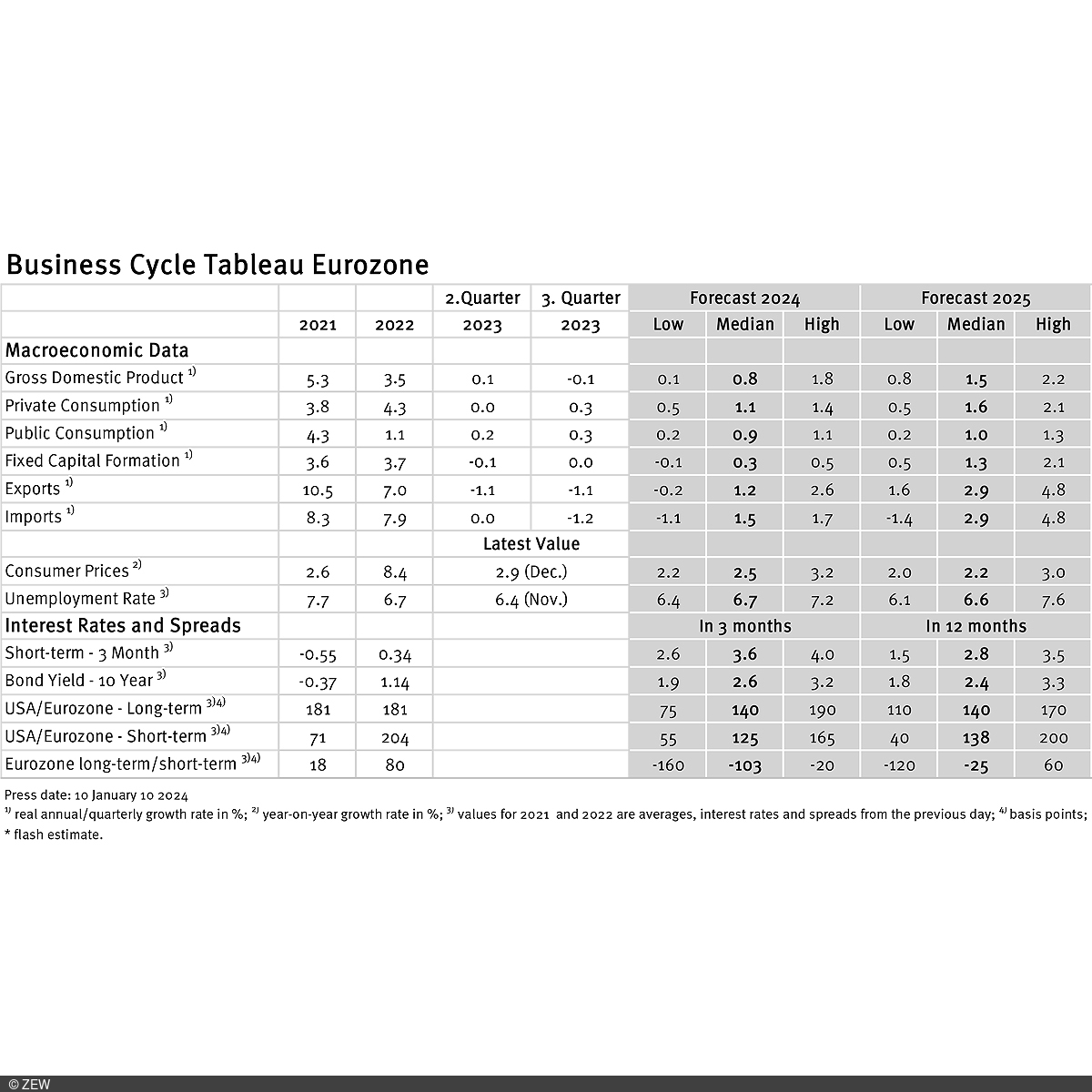

Business cycle experts are less optimistic about the development of Germany’s economy. The forecast for 2024 stands at a modest 0.4 per cent, possibly influenced by the Federal Constitutional Court ruling and rising inflation. Despite differences of opinion among experts, German foreign trade offers positive prospects for 2025. Expectations for the eurozone, however, remain subdued. These are the results of the business cycle tableaus by ZEW Mannheim and the German daily newspaper, Börsen-Zeitung.

The quarterly growth figures for Germany’s real gross domestic product (GDP) are given as 0.1 per cent for the second quarter and minus 0.1 per cent for the third quarter. For the entire year 2024, experts predict a 0.4 per cent increase in German GDP, 0.2 percentage points lower than the estimate from December. These slightly more pessimistic expectations may be due to the recent Federal Constitutional Court ruling on the debt brake, as well as the recent rise in inflation, which has dampened expectations of imminent ECB rate cuts. Significant disagreement among experts is evident, with a range of individual growth expectations spanning 3.8 percentage points. For 2025, a notably higher economic growth of 1.2 per cent is expected, primarily driven by German foreign trade. Growth rates of 2.9 per cent are anticipated for both the import and export sectors.

Forecasts for 2024 slightly downgraded, but optimistic outlook prevails for 2025

Quarterly growth figures for the eurozone mirror those of Germany, with 0.1 per cent in the second quarter and minus 0.1 per cent in the third quarter. Eurozone growth expectations have become somewhat more pessimistic. Experts have revised their growth forecast for 2024 downward by 0.1 percentage points to a new value of 0.8 per cent. For 2025, economic growth of 1.5 per cent is expected. Similar to expectations for Germany, forecasts for 2025 are significantly more optimistic than those for 2024. However, expectations for the eurozone for both years are considerably higher than corresponding forecasts for Germany.

Economists anticipate moderate growth in 2024 and are optimistic about the ECB approaching its target in 2025

After a recent significant decline, inflation rates in both Germany and the eurozone are showing an increase in December. Specifically, inflation rates of 3.7 per cent for Germany and 2.9 per cent for the eurozone were recorded, each 0.5 percentage points higher than the December values. For the entire year 2024, inflation rates of 2.8 per cent (Germany; up 0.1 percentage points from December) and 2.5 per cent (eurozone; down 0.3 percentage points from December) are expected. The recent inflation increase is thus not (yet) reflected in respondents’ expectations. Projected inflation rates for 2025 stand at 2.2 per cent for both Germany and the eurozone. Experts thus expect inflation to move significantly closer to the ECB’s inflation target in the coming year.

Meanwhile, expectations for short-term interest rates have increased by 0.1 percentage points to 3.6 points. Therefore, despite the expectation of further declining inflation rates, experts do not anticipate a near-term easing of monetary policy. However, the expectation for 2025 is significantly lower at 2.8 points compared to the value for 2024.

Business Cycle Tableaus by ZEW and Börsen-Zeitung

In cooperation with Börsen-Zeitung, ZEW has been publishing monthly business cycle tableaus for Germany and the eurozone with economic key figures and forecasts since 2013. Numerous banks and institutes publish reports on the current and prospective economic situation at different intervals. The information relevant for the tableau is filtered out of these publications to compute a median, minimum and maximum of the available forecasts for the current and subsequent year.

The monthly tableaus show current GDP forecasts, the expenditure breakdown, consumer prices, industrial production, unemployment rate, short- and long-term interest rates, and interest rate differentials (IDRs). The focus of the tableaus lies on national business cycle reports, which are complemented with forecasts from international banks and institutes. The tableau for the eurozone is enhanced by data from European banks and institutions.