Mechanical Engineering Sector Benefits Most from R&D Tax Credit and Sees Greatest Potential

ResearchZEW/VDMA Study the German R&D Tax Credit

By far the most applications for the newly introduced German R&D tax credit have so far been made by companies from the mechanical engineering sector. Within manufacturing, every third applicant for the tax credit was from this sector. Almost all mechanical engineering companies that have filed an application plan to use the additional funds to strengthen their research activities. This is the result of a recent survey among mechanical engineering companies by ZEW Mannheim and the German Mechanical Engineering Industry Association (VDMA). At the same time, many companies eligible for the R&D tax credit have not yet applied for it or lack information on how the application process works, what effort it entails and whether it is worthwhile, according to the study’s findings. The goal must therefore be to provide more information and to offer businesses assistance in the application and approval process. In addition, it must be defined more precisely for which R&D expenditures the tax credit can be claimed.

“The mechanical engineering sector is in the lead when it comes to taking advantage of the new innovation allowance,” emphasises Hartmut Rauen, deputy managing director of the VDMA. “The additional funds are spent on innovations. Transformation processes, e.g. the development of climate-neutral production, can thus be tackled even more actively. It is also clear that we must do everything we can to ensure that the R&D tax credit generates the best possible outcomes in practice,” says Rauen.

More than 60 per cent of the eligible companies in the mechanical engineering sector had not yet planned to apply for the R&D tax credit in autumn 2021. This corresponds to around 2,150 companies. According to ZEW calculations, just under 500 companies in the mechanical engineering sector had submitted an application to the relevant authority, another 200 or so were in the application process and around 600 were planning to submit an application. 83 per cent of the applications already submitted were approved. A total of about 3,400 companies in the mechanical engineering sector are eligible for funding.

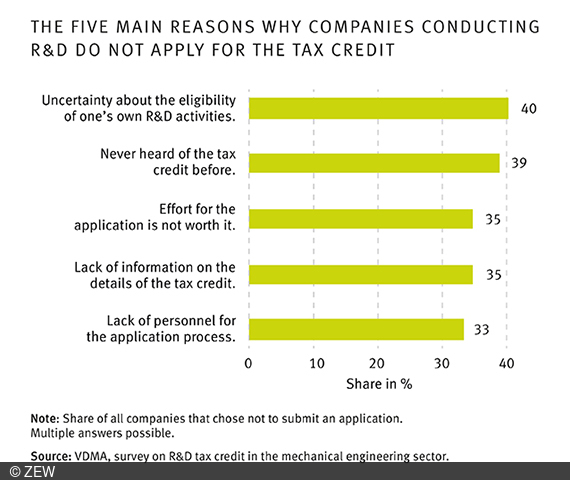

The main reasons for the high level of reluctance are a lack of information (39 per cent), uncertainty about the eligibility of one’s own R&D activities (40 per cent) and an application procedure that is perceived as too time-consuming (35 per cent). “Tax-based research funding is a relatively new policy instrument. The existing obstacles will diminish as more information about how the tax credit works becomes available and as eligible businesses gain more experience,” says Dr. Christian Rammer, researcher in ZEW’s “Economics of Innovation and Industrial Dynamics” Department and project head.

In addition, companies have up to four years to apply for a project’s eligibility with the relevant authority and then for the tax credit with the tax office. “The pandemic was and is a major challenge for many companies, also in terms of research and innovation,” emphasises Dr. Ralph Wiechers, head of the VDMA Tax Department. “Thanks to a generous submission deadline, the application for the research allowance did not have to be sent immediately and allowed other things to take priority in the company’s operations. But companies have to be careful not to forget about it due to the postponement,” warns Wiechers.

Companies need assistance

The biggest challenge for companies when applying is outlining the content (57 per cent) as well as the timeline and financial and human resources for the R&D project (43 per cent). To encourage more companies to apply, advisory bodies should provide more information about the new funding instrument and offer concrete assistance in the application and approval process.

“The current design of the tax credit also needs conceptual improvement in order to fully develop the desired innovation effect,” emphasises Christian Rammer. Overall, the administrative burden for the application procedure should be significantly reduced. A more practice-oriented definition of R&D would be desirable, as would the requirement for only a condensed presentation of R&D activities. “From an innovation policy perspective, tax-based R&D funding should provide quick and non-bureaucratic access to ‘basic funding’ for R&D activities that is manageable and that companies can take into account when deciding to what extent they want to carry out R&D activities,” says Christian Rammer.

Despite the cap on the assessment basis having been raised to four million euros per company until the end of 2025, funding is fairly limited even for larger, research-intensive SMEs. “In view of the government coalition’s goal of spending a total of 3.5 per cent of GDP on R&D, it is necessary to provide even more support for larger SMEs and thus increase the attractiveness of Germany as a business location for them,” Rauen emphasises.

350 mechanical engineering companies surveyed

Since April 2021, companies can claim the R&D tax credit. Companies that conduct research are entitled to an allowance of 25 per cent of their wage costs for research staff. In addition, they may receive an allowance of 25 per cent for contract research based on 60 per cent of the contract sum. For the study, the researchers surveyed around 350 companies in the mechanical engineering sector in September and October 2021 and used data from the authority that administers the R&D tax credit applications.