M&A Report: Concentration in European Landline Communications Network Increasing

M&A Index

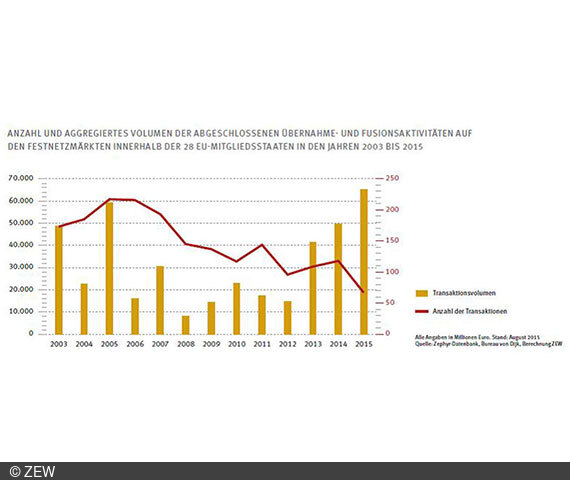

For years, a significant trend towards consolidation has been observed in the landline communication (fixed-link) market in Europe. The number of mergers and acquisitions (M&A) continues to fall and has recently reached its lowest level since 2003. In the last two years, however, there has been a massive increase in the aggregated volume of transactions, as it is principally larger firms which are now merging with one another. These are the findings of an analysis carried out by the Mannheim Centre for European Economic Research (ZEW) on the basis of the Zephyr database of Bureau van Dijk (BvD).

In addition to larger mergers between cable network providers, M&A activities have also involved providers of landline and mobile network services, as firms aim to combine these two infrastructure components. These transactions are in part due to increasing customer demand for fully integrated product bundles.

The process of combining voice and data communication in a single IP-network (IP-convergence), via which many services can be offered on a single platform, also forces landline providers to alter their business models. This in turn further increases competition pressure.

The last few years have also seen adaptations in the business models of telecommunications providers, including contractual agreements with content providers to ensure, for example, the pre-installation of customer-relevant applications (Apps). This trend is seen predominately in the mobile communications sector. Mobile communications products, however, face increasing competition from fixed-link telephone and broadband services.

For more information please contact

Dr. Wolfgang Briglauer, Phone +49(0)621/1235-279, E-mail briglauer@zew.de