Value Added Tax

Reduced VAT Rates: Scale Back Rather Than Expand

What policy recommendations arise from an analysis of the current system of reduced VAT rates? On behalf of the German Federal Ministry of Finance, a team from the ZEW Research Unit “Corporate Taxation and Public Finance” conducted a criteria- based evaluation of the main reduced VAT rates and analysed possible reform options along with their distributional and systemic effects.

(Friedrich Heinemann, Daniela Steinbrenner, Zareh Asatryan, Albrecht Bohne and Karina Kindler (from left to right))

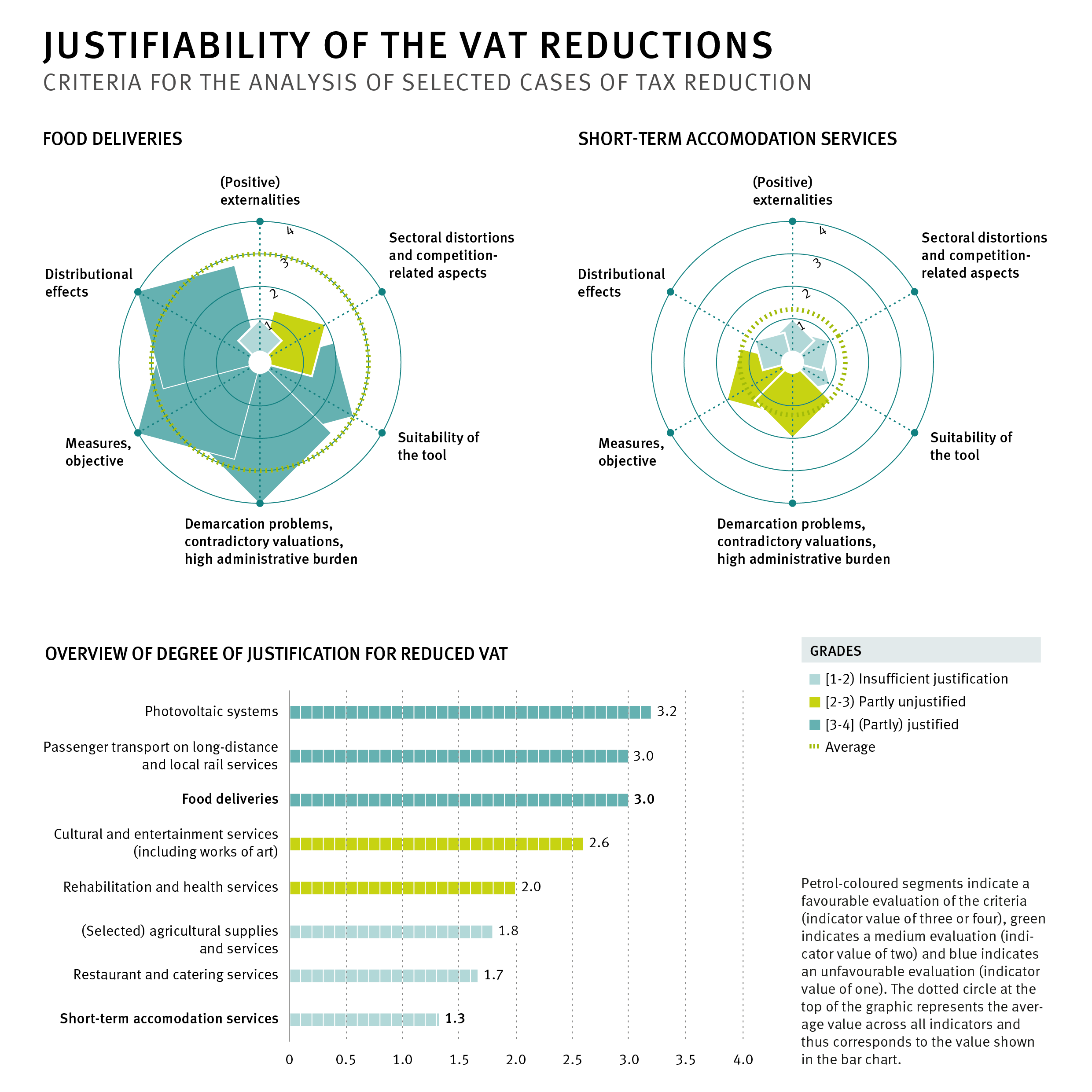

While Value Added Tax (VAT) remains a crucial source of revenue for the state, the current system, characterised by numerous reduced rates, is facing significant criticism from both economic and administrative standpoints. On behalf of the Federal Ministry of Finance, a research team from ZEW has evaluated the most significant aspects of the system using a criteria-based approach. The researchers examined whether the existing tax benefits are justified by sound arguments, for example, because they provide relief for low-income households or safeguard competitiveness. The evaluation was based on several criteria, including objectives, suitability of the tool of VAT reduction, distributional effects, administrative costs, positive externalities and competition-related aspects.

The analysis shows that only a few cases of reduced VAT rates are convincing. For instance, reduced rates for food – the largest reduction in terms of subsidy volume – do provide relief for lower-income households. Nevertheless, a targeted transfer policy would generally be more efficient and cost-effective. In contrast, other tax reductions prove to be significantly less justified. Especially in the case of short-term accommodation services there is no evidence of substantial benefits for lower-income households or relevant positive externalities, nor is there evidence of international competitive pressure. A similarly unfavourable assessment was given to the VAT reduction for selected agricultural and forestry supplies, whose B2B nature and overlap with the reduced VAT rates for food make a distributional effect unlikely.

The experts surveyed additionally emphasise that differentiated tax rates lead to significant systemic problems. The multitude of exceptions increases the administrative burden, creates legal uncertainty and encourages tax evasion. Furthermore, a structural incentive for lobbying arises, leading to a ‘spiral of benefits’.

The ZEW researchers therefore evaluate three revenue-neutral reform options. A complete abolition of all reduced rates would lower the standard rate to 16.74% but place a disproportionate burden on the poorest households. The effects of two alternative proposals are significantly more moderate: Retaining the reduced VAT rate for food while abolishing all other reductions lowers the rate to 18.14%; the third option – the abolition of reduced rates for restaurant, catering and accommodation services – results in a rate of 18.55%. The additional burden for the poorest decile would be close to zero, and for wealthier households it would be relatively greater.

Conclusion: The researchers recommend a new concept for the VAT system. A leaner, more transparent system with few, systematically justified exceptions would promote efficiency and administrative simplification. The study findings suggest that VAT should be restored to its original purpose (i.e. a broad-based consumption tax) and that sector-specific special rules should be replaced by more targeted instruments within the transfer system. A gradual phasing out of the numerous reduced-rate provisions is therefore urgently needed to reduce distortions and strengthen the coherence of the tax system.

Corporate Taxation and Public Finance

The “Corporate Taxation and Public Finance” Research Unit addresses questions related to corporate taxation and empirical public economics within the context of European integration.

Contact

Prof. Dr. Friedrich Heinemann

Head Email friedrich.heinemann@zew.de Phone +49 (0)621 1235-149