Economic Outlook Remains Positive in the German Information Economy

Information Economy

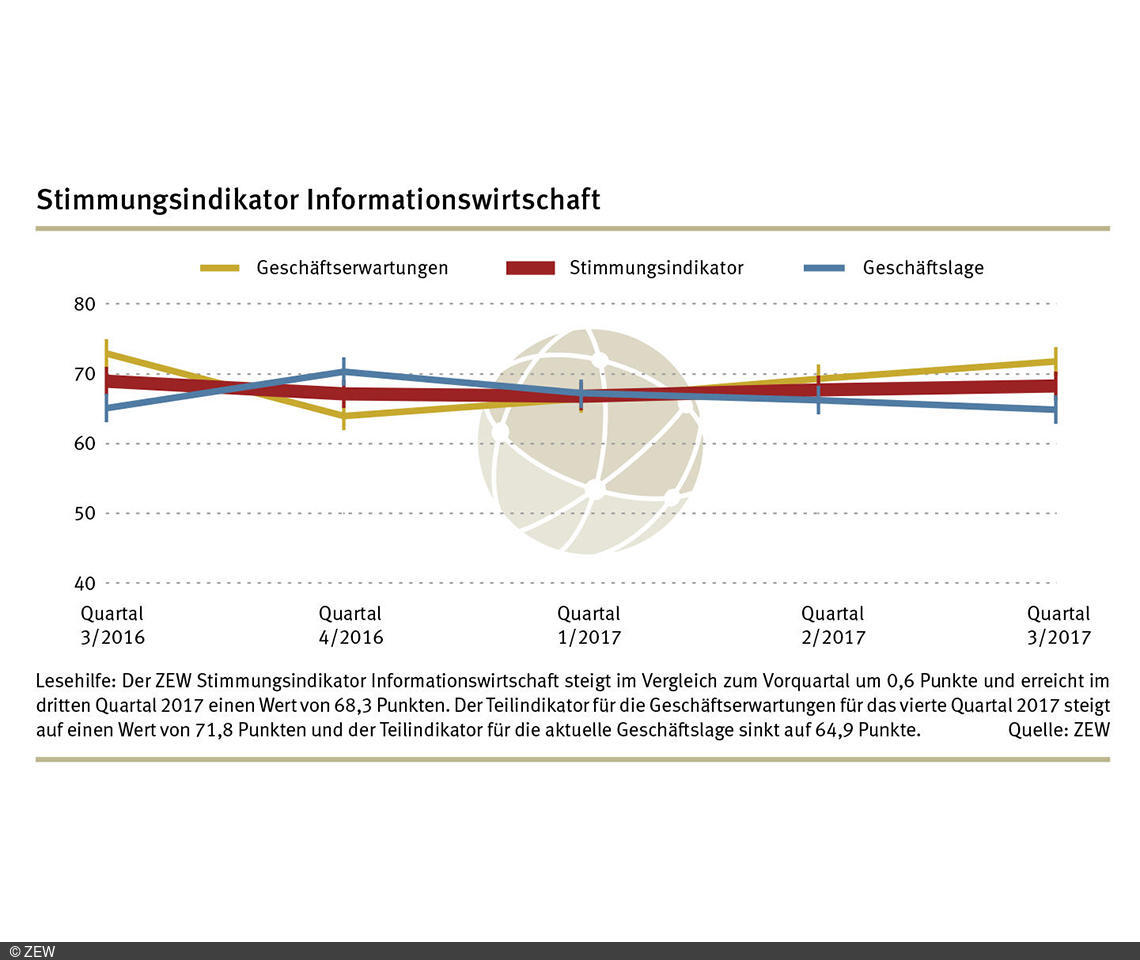

Economic sentiment among companies in the German information economy sector has been largely positive in the third quarter of 2017, as suggested by the ZEW Sentiment Indicator for the Information Economy. The indicator takes into account the companies’ current business situation as well as their business expectations. In comparison to the previous quarter, the sentiment indicator has climbed 0.6 points to a current level of 68.3 points. This is the result of a survey conducted among firms in the German information economy by the Centre for European Economic Research (ZEW), Mannheim, in September 2017.

The increase in the sentiment indicator was driven by the positive development of the firms’ business expectations for the fourth quarter of 2017. The corresponding sub-indicator has increased by 2.5 points compared to the previous quarter, reaching a total of 71.8 points. In surpassing the critical 50-point mark by a considerable margin, the indicator reflects that the majority of companies are anticipating both higher turnover and demand for their products and services in the fourth quarter of 2017. The sub-indicator for the business situation has also closed well-above the 50-point mark in the third quarter of 2017. Despite a slight drop by 1.3 points, the sub-indicator has reached a total of 64.9 points.

The information economy consists of the sub-sectors information and communication technologies (ICT), media service providers, and knowledge-intensive service providers. In the current survey, ICT companies have retained their extremely positive economic sentiment. Starting from an already high level, the sentiment indicator has climbed further by one point and currently stands at 73.3 points. Meanwhile, the sub-indicators for the business situation and for the business expectations have, however, started to develop in opposite directions. Business expectations have improved considerably in comparison to the second quarter. By contrast, the sub-indicator for the business situation has experienced a decline, falling by 2.9 points compared to the previous quarter. The sub-indicator’s current reading of 67.1 points nevertheless suggests that the majority of companies performed well in the third quarter of 2017. On balance, around 32.1 per cent of businesses were able to increase their turnovers. According to the surveyed firms, the demand for products and services has been equally positive. Besides their positive assessment of the business situation, companies are particularly optimistic about their business expectations for the fourth quarter of 2017, with the corresponding sub-indicator reaching a level as high as 80.1 points.

Media service providers also stay positive

The economic mood among media service providers is also positive in the third quarter of 2017 with the corresponding indicator falling by 2.2 points to a current reading of 55.8 points. The indicator, however, still remains far above the critical 50-point mark. After having dropped 2.1 points, the sub-indicator for the business situation has remained just over the crucial 50-point mark and currently stands at 50.1 points. The overall economic outlook, however, continues to be positive among media service providers. Despite a decline by 2.3 points, the sub-indicator for business expectations has reached a total of 62.2 points. On balance, 21.9 per cent of firms expect demand for their products to increase, while as many as 27 per cent anticipate a higher turnover for the fourth quarter of 2017.

The assessment of the economic situation among knowledge-intensive service providers also remained very positive in the third quarter of 2017. The sentiment indicator for the knowledge-intensive service providers already reached record levels in the last two quarters. The indicator has now once again risen by 1.1 points, reaching 67.3 points – its highest level in a long time. The companies’ assessment of both the business situation and expectations have also developed positively compared to the previous quarter. The sub-indicator for the business situation currently stands at a level of 66.5 points, while the sub-indicator for business expectations has reached a total of 68.1 points.

For further information please contact

Dr. Daniel Erdsiek, Phone + 49 (0)621/1235-356, E-mail daniel.erdsiek@zew.de

The Economic Sentiment Indicator in the Information Economy

The Economic Sentiment Indicator for the Information Economy is composed of the four components sales situation, demand situation, sales expectations and demand expectations (each in comparison with the previous and following quarter). They are equally taken into account for the calculations. The sales situation and the demand situation form a sub-indicator reflecting the business situation. Sales expectations and demand expectations form a sub-indicator reflecting business expectations. The geometrical mean of the business situation and the business expectations is the value of the Economic Sentiment Indicator in the Information Economy. The sentiment indicator can take on values from 0 to 100. Values above 50 indicate an improved economic sentiment compared to the previous quarter, values smaller than 50 indicate deterioration compared to the previous quarter.

The ZEW Business Survey in the Information Economy

About 5,000 businesses with a minimum of five employees participate in the quarterly survey conducted by ZEW. The companies surveyed belong to the following business sectors: (1) ICT hardware, (2) ICT service providers, (3) media, (4) law and tax consultancy, accounting, (5) public relations and business consultancy, (6) architectural and engineering offices, technical, physical and chemical analysis, (7) research and development, (8) advertising industry and market research, (9) other freelance, academic and technical activities. Combined, all nine sectors make up the economic sector of the information economy. The ICT sector consists of ICT hardware and ICT service providers. Sectors three to nine make up the knowledge-intensive service providers. Overview of the ZEW Business Survey in the Information Economy (in German): www.zew.de/konjunktur.